Last month I had the opportunity to attend the ITW Telecommunications Week conference in Atlanta, GA. One of the major topics from the show was the announcement of a consortium of telecommunication companies and software companies converging to develop a blockchain solution that will create a “frictionless” payment settlement process across the telecommunications sector.

All of this is the culmination of several Proof of Concept projects conducted over the past year through organizations such as the Metro Ethernet Forum (MEF), whose focus is to facilitate the development of agile, assured, and orchestrated services for the Communication Service Provider (CSP) Industry.

The TM Forum, another group focused on bringing telecommunication companies together, is actively pursuing their own projects through their Catalyst Program. Several of these projects are blockchain focused, and have delivered impressive results, such as demonstrating the ability to quickly provision telecommunication assets for short-term or long-term needs.

Clearly the telecommunications sector is taking blockchain seriously, and making investments around the technology—but what is blockchain, and how can it help the industry?

What is a blockchain?

If you are looking for an official definition of blockchain, look no further than Wikipedia:

“A blockchain, originally block chain, is a growing list of records, called blocks, which are linked using cryptography.”

Source: Anand, S. and Sinoj Maxwell (2017, Nov 22). Blockchain! Say What?, Retrieved from https://medium.com/hashtaagco/blockchain-say-what-8e16ed29e543

The records (or transactions) in a given block can be anything: changes in real estate titles, the custody chain of a tuna fish from the moment it was caught to the time it was sold to a restaurant, or the transfer of a bitcoin from one address to another.

But creating a collection of transactions and inserting them into inter-linked blocks is only one aspect of the blockchain. Some of the other characteristics of a blockchain are that it is:

- Decentralized—Blockchains do not rely on a central point of control to validate transactions and record data. Instead, they employ incorruptible consensus protocols across a network of nodes.

- Immutable—Transactions cannot be changed once they have been recorded and written to a blockchain. This is one of the primary differences between blockchain and traditional databases where, with the right permissions, rows and columns (and data) can be easily altered, added, or deleted.

- Trustless—Blockchain is a “trustless” system, which means that one does not have to trust another to complete a transaction. For example, if someone gives a person $10, the recipient knows the $10 is now theirs to spend. Alternatively, if someone uses a credit card for a purchase, there is a chance the credit card gets declined. A certain level of trust is required for credit transactions, but trust is fully embodied within blockchain transactions; and

- Disintermediation—Blockchain operates without a middle man. There is no bank or broker to collect a fee as part of a transaction.

Union Square Ventures in New York City has an interesting take on blockchain. They posit that the protocols we have right now—such as HTTP, TCP/IP, SMTP—have obtained tremendous value because they are the protocols on which larger applications like Google, Amazon, Facebook and Apple have built their own applications.

With blockchain, however, the value is in the protocol itself (the blockchain), and much less value is inherent to the application. Read the full “Fat Protocols” article, Union Square Ventures’ take on blockchain and the concept of tokens (e.g. Bitcoin).

How does it work: the simple version

Blockchain is a distributed technology. Whether it’s a public blockchain, or a more controlled permissioned/consortium blockchain, every node (or participating computer) has an exact copy of the blockchain program. You can choose to be a node on the blockchain network, or simply a user of the blockchain.

Let’s go through a simple example of how someone might use the Bitcoin (BTC) blockchain. Joe wants to send 0.1 BTC to Anne. Using a Bitcoin exchange or a Bitcoin wallet, Joe will initiate a transaction by including Anne’s address and the Bitcoin amount that is to be transferred.

Note: the address is a hashed representation of the recipient’s public key, which is something beyond the scope of this document.

Once Joe submits his transaction, it will first be validated (this is a complicated but important step), then bundled with other transactions and loaded into a block. The block is then inserted into the complete blockchain by miners who compete for the right to insert the block. They go through a “proof of work” task to earn the right to add the block, and are awarded by receiving a sum of bitcoin (approximately 12.5 BTC). At this point, the transaction is added and is now immutable, which means that is almost impossible to alter the transaction.

How does it work: the deeper dive

All blockchains make extensive use of cryptography and hashing to process and secure transactions. Both cryptography and hashing are used to: (1) verify ownership and availability of monetary assets for every transaction, and; (2) safely secure these transactions as blocks.

Hashes and public/private key pairs are used to verify ownership and asset availability. Should “Anne” initiate a transaction, the wallet she uses takes the information about the transaction, including the transfer amount and the recipient’s address, and create a hash of that information. This hash is then encrypted using the private key, which creates a unique digital signature for Anne (the sender).

The signature and the hash (which contains the transaction information) are then sent out to the blockchain for verification. On the receiving end, one or more nodes will take the encrypted hash and use Anne’s public key to decrypt it to produce a 256 bit hash. If that hash matches the hash that was sent along with the encrypted file, the node can verify Anne sent the transaction. The node then reviews past transaction records matching Anne’s public key to ensure that she has enough BTC to transfer.

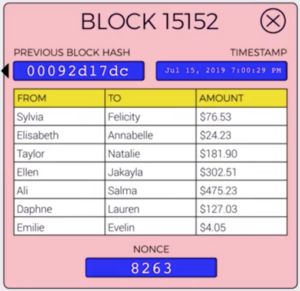

But what about the blocks themselves? How is a blockchain actually formed?

Each block contains several elements:

- The block ID;

- The transactions that are part of the block;

- The previous block’s hash;

- A merkle root;

- A timestamp; and

- This strange thing called a nonce.

I won’t get into how a block is created and validated, except to briefly say that it revolves around the concept of “proof of work,” and involves BTC mining, which you’ve probably heard about.

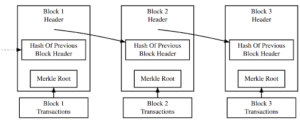

What I want to focus on here is what makes it secure. It really boils down to one elegant technique—each block in a blockchain is connected to the previous block by the previous block’s hash.

What does this mean? This means that it is impossible to tamper with the contents of a specific block without affecting the entire blockchain. Take the diagram below for example; if I were to try to change any of the transactions in Block #1, it would change the hash of that block and affect subsequent blocks (e.g. Blocks #2 and #3). All the while, new blocks are being added that depend on the hash values of all the blocks before them. It would take a really powerful computer to keep up enough to pull off tampering with the blockchain, which is why blockchain transactions are considered immutable.

Simplified Bitcoin Blockchain

What are the benefits of blockchain technologies?

Blockchain technologies are poised to significantly change the way we make transactions. Coupled with smart contracts and automated services, it may very well become the mechanism we use to access and use IoT devices and products.

With blockchain technologies, we can eliminate the “middleman” as well as the risk or inconvenience of transactions being held up or canceled. Additionally, we can use smart contracts to facilitate the secure and efficient transfer of tokenized assets from one entity to the next.

Finally, blockchain technology provides the opportunity to decentralize systems that have historically been controlled by a single entity. The data is distributed amongst all members in the blockchain which, through consensus mechanisms, ensures that individual data is safe and handled in mutually agreed upon ways.

How is blockchain being used today?

Several businesses and industries have been testing and deploying blockchain technologies.

Real estate is a prime candidate for deployment, and increasingly more examples of implementation are surfacing. Recently, Cook County Illinois launched a blockchain pilot program to help record and organize the tremendous number of documents their courthouses are required to store and manage. There’s also Meridio, a relatively young company using blockchain to make it easier for multiple shareholders to own a single property.

Energy is another sector ready for blockchain. Companies like Grid+ are connecting end users with electricity providers, handling the billing and metering, and effectively eliminating the role of resellers. Power Ledger, an Australian company, is looking at blockchain technologies to enable energy sharing amongst peer-to-peer, community-based energy grids.

Food safety, carbon reduction, pharmaceutical retail, supply chain management, voting and, of course, banking, are other sectors where we will likely see use of blockchain technologies.

There has also been some activity in the Communication Service Provider (CSP) space, particularly amongst carriers that are looking for a way to employ a single system to handle inter-carrier transactions for voice and data services. There’s still a lot to develop in this space, and the VETRO FiberMap team is considering ways to add value, so stay tuned.

Conclusion

When Sataoshi Nakamoto introduced blockchain technology to the world in his 2008 Bitcoin White Paper, it was unclear how it would be used beyond a means to exchange cryptocurrency. There is, however, an increasing groundswell of support for this technology. Despite well known obstacles to scaling blockchain technology, groups such as the Enterprise Ethereum Alliance are working hard to make it more mainstream. Perhaps some day we will all be transacting on one or more blockchains for our most basic needs.

Author: Sean Myers

Co-Founder | COO

VETRO FiberMap

email | phone | LinkedIn